If you are concerned about losing your home because you cannot make your mortgage payments, contact us about our Foreclosure Prevention program. CRC partners with homeowners who are struggling to meet the costs of keeping their homes by working with banks and community organizations to create options which meet the needs of all involved.

Download the documents you need to participate in our Foreclosure Prevention or Housing Lottery programs below:

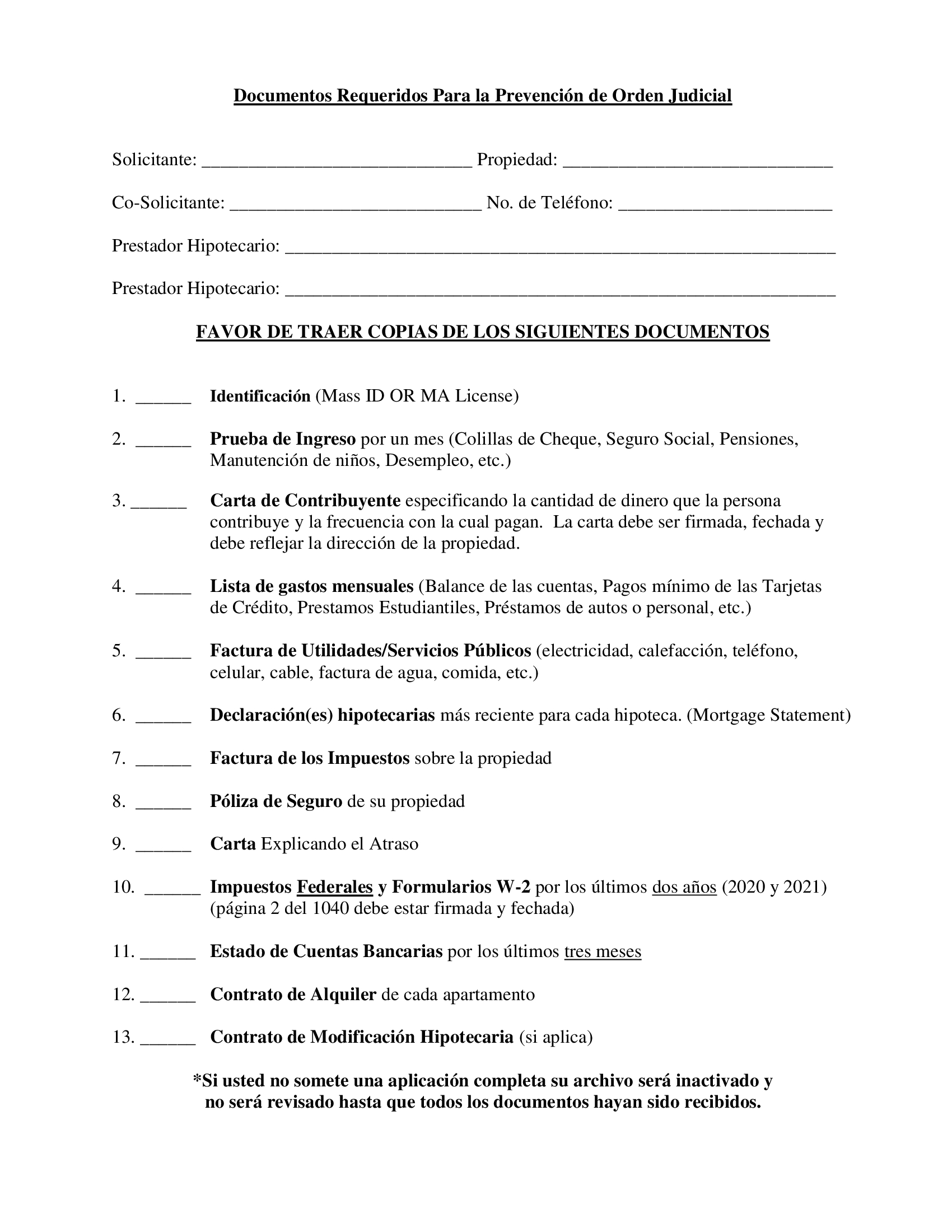

Required Documents for Foreclosure – Spanish

{kind=link}

{kind=link}

Required Documents for Foreclosure English

Foreclosure Prevention Flyer’s

BEWARE OF SCAMS/FRAUD!!

Fannie Mae Beware of Scams

How to Avoid Housing Scams

It’s not uncommon for scammers to try to take advantage of homeowners in crisis through a foreclosure rescue scam, foreclosure relief scam, mortgage company scam, or others.

![]()

If you receive an offer, information, or advice in a time of crisis, and it sounds too good to be true, then it probably is. These key do’s and don’ts can help you identify, avoid, and report possible scams.

![]()

Do

- Ask questions — for example: How did you get my contact information? Can I see your identification or business license? Can you send me written information to review?

- Confirm identities — know the people or organizations you’re working with.

- Confirm contracts — make sure written contracts match any verbal promises.

- Protect your identity — avoid giving out personal information, like your credit card info or social security number.

- Stay up to date — know the most prevalent scams going on in your area.

![]()

Don’t

- Share your personal or financial information over the phone or via email and text messages.

- Make decisions under pressure — instead, be sure to read and understand everything before taking any action.

- File mortgage payments to anyone other than your servicer (the company that receives your monthly payments) — and do not file without your mortgage company’s approval.

- Sign unknown papers — for instance, if they promise that someone else will pay off your mortgage or anything else that requires a written agreement.

- Blindly trust a representative’s authority — whether they say they’re from the government or your mortgage servicer, the person who contacted you may not actually be from the organization they claim to be from.

- Pay to modify your mortgage — remember, housing counseling and adjustments to your agreement through your servicer are always free.

Common homeowner scams

By staying aware of common local and national scams, such as the “foreclosure rescue scam,” you can avoid falling victim to fraud.

Foreclosure rescue scam

- Scammers promise to negotiate with your lender to modify your loan or save your house, posing as a counselor.

- They will request a fee and may tell you not to contact your lender, assuring you that they’ll handle everything.

Remember: It is free to work with your lender or a HUD-approved housing counselor, so consider any requested fees to be a red flag.

FEMA fraud

- Imposters will pose as a FEMA representative after a disaster and ask for money.

- FEMA will never request or accept money, and all FEMA associates, including home inspectors, have a laminated photo ID.

Remember: Call FEMA at 1-800-621-3362 to confirm a FEMA representative’s identity.

Mortgage/home loan scams

- Scammers may offer help with or promise to delay your loan payments.

- Always work directly with your mortgage servicer — never pay for someone to “negotiate on your behalf.”

Remember: Working with a HUD-approved housing counselor or your lender is always free, so consider any requested fees to be a red flag.

Report possible scams

If you think you’ve been impacted by a scam, submit a report to the following organizations.

- Fannie Mae’s Mortgage Fraud Report

- FEMA Fraud Report

- The Federal Trade Commission (1-877-382-4357)

- Your state’s attorney general or another local authority.

A HUD-approved housing counselor is the most trusted, safest source of information and help.

Remember that they will never ask for or accept money.

Talk to a housing counselor at no cost to you!

Call 1-855-HERE2HELP (855-437-3243),or schedule an appointment.

Freddie Mac Refinancing

Understanding your options for refinancing

There are two primary options for refinancing your mortgage, each with its own costs and benefits.

If you are considering refinancing your mortgage, there are two primary options you’ll need to choose between: no cash-out refinance and cash-out refinance. Each is designed to meet specific goals. But be sure to talk with your lender about the costs and benefits of each option as refinancing will require both time and money.

No cash-out refinance

With a no cash-out refinance, you are primarily refinancing the remaining unpaid balance on your mortgage. This is the most common option and may make sense if you’re looking to:

- Lower your mortgage rate. If mortgage rates are lower than when you closed on your current mortgage, refinancing could reduce your monthly payments and the total amount of interest that you pay over the life of the loan.

- Move from one mortgage product to another. If your current mortgage is an adjustable-rate mortgage (ARM) and it no longer makes sense for your financial situation, refinancing into the security and stability of a fixed-rate mortgage may be a good decision.

- Build equity faster. If your financial situation has improved since your purchase, refinancing to a loan with a shorter term (e.g., from a 30-year fixed-rate mortgage to a 15-year fixed-rate mortgage) will allow you to build equity faster, own your home sooner and pay less in total interest.

Cash-out refinance

If you’ve built up significant equity in your home over the years and could use funds for home improvements or to improve your financial situation, a cash-out refinance may make sense for you.

With a cash-out refinance, you’re refinancing your mortgage for more than you currently owe. In return, you’re getting a portion of your equity back in cash. Cash-out refinances generally have a slightly higher mortgage rate because you are borrowing more money, which is an added risk to the lender making the loan.

If you’re thinking about a cash-out refinance for home renovations, learn more about our CHOICERenovation® mortgage and CHOICEReno eXPress® mortgage.

Speak to your lender to discuss your refinance options. Consider meeting and comparing multiple lenders to determine which lender offers the best terms and cost.

Remember, your new loan will have a new rate and term, and you’ll be responsible for all costs associated with the refinance.

You must be logged in to post a comment.