Down below you will see a list of down payment assistance programs with any information you need to apply.

First Time Homebuyer Down Payment Assistance Loan Program (NSC)

North Suburban Consortium c/o Malden Redevelopment Authority

The North Suburban Consortium (NSC) offers Down Payment Assistance loans (DPA) to income eligible First Time Home Buyers (one who has had no homeownership interest in a principal residence during the past 3 years OR a displaced homemaker or single parent who has only owned a home with a former spouse while married) (FTHB) purchasing a condominium, townhome or single-family property in one of the eight NSC communities. DPA can be used to assist with the down payment and customary closing costs, however, it cannot be used for reimbursement for previously paid earnest money down payment; funding monthly housing payment reserves requirements; prepayment of life insurance premiums; or to bridge the gap between purchase price and appraised value. Applicant’s primary mortgage lender must agree to fund DPA amount at closing and accept reimbursement after closing. Applicants cannot receive money back at closing.

Effective July 1, 2024, DPA can be up to $10,000.00 for non-subsidized property and for NSC HOME-subsidized property, up to $5,000.00 (amount determined at completion of underwriting). DPA is a 0% interest, 5 year deferred loan. Each anniversary date, 20% of the original DPA is forgiven; in 5 years, the loan is completely forgiven (a mortgage discharge for recording at the registry of deeds will be mailed to owner). Owner must live in the property as their primary residence. NSC does not subordinate DPAs. If an owner refinances, sells, transfers or no longer resides in the property before the end of the loan term, they must repay a prorated portion of the DPA.

Please allow three to four weeks from date of submission for review of DPA Loan Application and supporting documentation, loan underwriting, required inspection, preparation of documents, contact with parties, primary mortgage lender, closing attorney, etc.

DPA Fact Sheet/ Checklist & Application Link

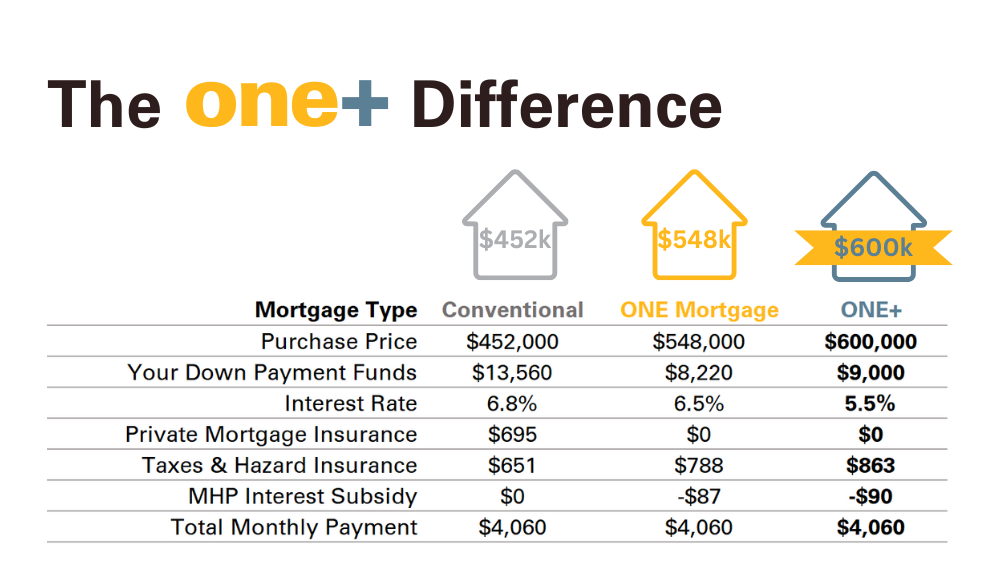

ONE+ Down Payment Assistance Program

The ONE+ Mortgage Program builds on the affordable features of the ONE Mortgage Program to deliver affordable financing solutions for low- and moderate-income first-time homebuyers currently residing within 29 Massachusetts communities. Specifically, the ONE+ Mortgage Program adds a permanent interest-rate discount, down payment and closing cost assistance.

Features of ONE+

ONE+ lowers the cost of buying and owning a home in Massachusetts by providing the same great ONE benefits…

- Heavily discounted, fixed, 30-year interest rates

- No private mortgage insurance (PMI)

- Lower down payment requirement

- Additional financial assistance for eligible buyers

…with these additional features unique to ONE+:

- Enhanced down payment assistance

- Closing cost assistance

Homebuyer Eligibility

To qualify for ONE+ you must:

- Be a current resident of one of the following cities: Attleboro, Barnstable, Boston, Brockton, Chelsea, Chicopee, Everett, Fall River, Fitchburg, Framingham, Haverhill, Holyoke, Lawrence, Leominster, Lowell, Lynn, Malden, Methuen, New Bedford, Peabody, Pittsfield, Quincy, Randolph, Revere, Salem, Springfield, Taunton, Westfield, or Worcester.

- Be a first-time homebuyer. This means that you have not owned a home at any point in the last three years.

- Take a homebuyer class. This class will help you get ready for the home buying process. We accept any class on this list.

- Meet our down payment requirements. We require a 3% down payment to buy a condo, single-family home, or two-family home.At least 1.5% of the purchase price must be from your own savings. For a three-family property, we require a 5% down payment with at least 3% from your own savings.

- Have a total household income under our limits. Income limits vary by the community you are considering purchasing in. Check your community on this page.

- Have less than $100,000 in total household assets. This includes any checking accounts, savings accounts, stocks, or bonds. But it does not include most retirement (401k, 403b, 457, traditional IRA) and college savings accounts. It also does not include the money you receive from down payment programs.

- Meet our credit score limits. Your credit score must be at least 640 to buy a single-family or condo and at least 660 to buy a two/three family home. We also have options for people who don’t have any credit history.

- Agree to live in the property as your primary residence. If you stop living in the property, you must refinance out of your ONE Mortgage.

MassHousing

Down Payment Assistance up to $30,000

Available with a MassHousing Mortgage for home purchases in every city and town in Massachusetts!

Saving for a down payment is one of the biggest challenges homebuyers face. That’s why MassHousing provides eligible homebuyers with Down Payment Assistance of up to $30,000 when purchasing a home in every city and town in Massachusetts.

Who is eligible for Down Payment Assistance from MassHousing?

To be eligible for Down Payment Assistance from MassHousing, you must

- Be an income-eligible first-time homebuyer

- Purchase a single-family home, condominium, or 2-, 3- or 4-family property that will be your primary residence

- Pair Down Payment Assistance with an affordable MassHousing Mortgage loan to purchase your home

Additional eligibility requirements apply. See if a MassHousing Mortgage with Down Payment Assistance may be right for you.

Not sure if MassHousing is right for you?

MassHousing mortgage loans and down payment assistance aren’t for everyone, but they’re available to more people than you might think.

Down Payment Assistance Details

MassHousing provides down payment assistance in the form of a second mortgage loan. MassHousing-approved lenders determine which type and the amount of down payment assistance a borrower is eligible for.

Option 1 DPA is an interest-free deferred payment second mortgage loan, which means that no payments are due until the property is sold, refinanced, or the first mortgage loan is paid off, at which time, the entire balance is due.

Option 2 DPA is a 15-year amortizing second mortgage loan at a fixed 2% rate of interest (APR 2%), which means that the borrower makes monthly payments of principal and interest for 15 years on this second loan, in addition to the monthly payments on their first mortgage loan.

| DPA Option | Repayment | Maximum DPA Amount | Home Purchased in | Interest Rate | APR | DPA Loan Must be Paid Off |

|---|---|---|---|---|---|---|

| 1 | Deferred | $30,000 | All communities in the Commonwealth of Massachusetts Subject to income and 1st Mortgage Program eligibility | 0% | 0% | Upon the sale of the propertyIf the first mortgage is refinancedIf the first mortgage is paid off |

| 2 | Amortizing (monthly payments required*) over 15 years | $25,000 | All communities in the Commonwealth of Massachusetts Subject to income and 1st Mortgage Program eligibility | 2% | 2% | Upon the sale of the propertyIf the first mortgage is refinancedIf the first mortgage is paid off |

*Payment Amount Example: A DPA loan in the amount of $25,000 would have 180 payments of $160.88.